Retail banking market investigation

Business current account and personal

current account pricing analysis

7 August 2015

This is one of a series of consultative working papers which will be published during the

course of the investigation. This paper should be read alongside the updated issues

statement and the other working papers which accompany it. These papers do not form the

inquiry group’s provisional findings. The group is carrying forward its information-gathering

and analysis work and will proceed to prepare its provisional findings, which are currently

scheduled for publication in September 2015, taking into consideration responses to the

consultation on the updated issues statement and the working papers. Parties wishing to

comment on this paper should send their comments to [email protected] by

Friday 21 August 2015.

© Crown copyright 2015

You may reuse this information (not including logos) free of charge in any format or

medium, under the terms of the Open Government Licence.

To view this licence, visit www.nationalarchives.gov.uk/doc/open-government-

licence/ or write to the Information Policy Team, The National Archives, Kew, London

TW9 4DU, or email: [email protected].uk.

The Competition and Markets Authority has excluded from this published version

of the working paper information which the inquiry group considers should be

excluded having regard to the three considerations set out in section 244 of the

Enterprise Act 2002 (specified information: considerations relevant to disclosure).

The omissions are indicated by []. Some numbers have been replaced by a

range.

1

Contents

Page

Introduction ................................................................................................................ 2

Business current accounts (BCAs) ............................................................................. 2

BCA prices ........................................................................................................................ 2

Customer profiles .............................................................................................................. 4

Methodology ...................................................................................................................... 5

Results .............................................................................................................................. 6

Interpretation of the analysis ............................................................................................ 11

Personal current accounts (PCAs) ........................................................................... 12

Appendix A: BCA credit interest rates, overdraft charges and customer incentives . 14

Appendix B: BCA customer profiles ......................................................................... 18

Appendix C: Figures by profile for the BCA monthly charge .................................... 20

Appendix D: Weighted average BCA price in Northern Ireland ................................ 23

Appendix E: PCA monthly price against market share ............................................. 25

2

Introduction

1. Appendix C of our updated issues statement (UIS) set out our approach to the

comparison of prices across personal current account (PCA) and SME

banking providers. We noted there were two main approaches to comparing

prices of complex bundled products such as PCAs and business current

accounts (BCAs):

(a) A bottom-up comparison of the amount paid by representative customers.

(b) A top-down comparison of net revenue per account.

2. In this paper, we provide an update on the bottom-up comparisons for BCAs

and PCAs.

1

Business current accounts (BCAs)

3. In this section we describe our comparisons of the monthly cost of BCAs for a

number of different customer profiles, based on published prices.

4. We asked the five largest banks to submit five representative BCA customer

profiles together with weightings showing the proportion of their BCAs that

these profiles reflected.

5. The following sections cover: BCA pricing, representative customer profiles,

our methodology for making comparisons, our results and a discussion of the

interpretation of our results.

BCA prices

6. BCAs, in their simplest form, provide everyday banking services to

businesses, similar to those provided to personal customers by PCAs. These

services are: payment transactions, store of value, and borrowing facilities

(overdrafts). However, not all BCA customers have an overdraft facility.

7. BCAs often include charges for transactional services and for use of overdraft

facilities. Some BCAs pay interest on in-credit balances. Appendix A sets out

information available on overdraft charges and credit interest rates.

1

The UIS included our ‘top-down’ revenue analysis for PCAs and BCAs, see UIS Appendix C paragraphs 15 to

21 and Annex 4. We noted in UIS Appendix C paragraph 21 that we were carrying out similar exploratory

analysis for other SME products. Any relevant results from this analysis will be included in our provisional

findings.

3

8. Our analysis covers charges for transactional services (including any monthly

charges) and focuses on BCAs identified by the banks in response to the

market questionnaire. We excluded BCAs aimed at a particular type of

enterprise, such as charities, clubs and societies as these account for a

relatively small proportion of all BCAs. Our analysis is also limited to current

BCA tariffs and excludes legacy tariffs. Many banks offer incentives to new

customers, which often differ between startups and switchers – details of

these incentives are set out in Appendix A.

9. Business banking transactions used in our analysis can be divided into

electronic transactions – such as auto credits and direct debits – and branch

transactions – such as depositing or withdrawing cash over the branch

counter. The analysis includes the most important transactions for which

pricing data was readily available.

10. We included the following electronic transactions:

(a) auto credit – an electronic credit paid into the account;

(b) bill payment – a bill payment which is debited to the account via

telephone or internet banking service and credited to a recipient;

(c) debit card – a debit to the account following a business debit card

payment;

(d) direct debit – a direct debit payment made from or returned to the

account; and

(e) standing order – a standing order payment made from the account.

11. We also included the following branch/other transactions:

(a) branch paying-in – credits paid in over the branch counter (containing

cash and/or cheques);

(b) branch withdrawal – cash withdrawal over the branch counter (ie when

cashing a cheque);

(c) branch cash-in – a charge in addition to the branch paying-in charge for

cash paid in at branch (as a percentage of the value deposited);

(d) branch cash-out – a charge in addition to the branch withdrawal charge

for cash withdrawal over branch counter (as percentage of the value

withdrawn);

4

(e) ATM cash-out – charge for debit associated with a cash withdrawal from

self-service machine (one debit per withdrawal) and an additional charge

for cash amount withdrawn from self-service machine (as a percentage

of the value withdrawn);

(f) cheques paid-in – a charge in addition to the branch paying-in charge for

cheques paid in at branch; and

(g) cheques issued – cheques written.

12. We used pricing data published on the Business Moneyfacts website in

January 2015.

2

Customer profiles

13. We asked the five largest banks

3

to submit five transactional profiles

4

which

were broadly representative of their SME BCA customers on standard tariffs,

together with weightings showing the proportion of BCAs that these profiles

reflected.

14. We asked the banks to exclude SMEs with an annual turnover larger than £2

million as these SMEs tend to negotiate their prices and, therefore, published

prices are less relevant to this segment.

15. According to one bank ([]), approximately [] of all transactions (by

volume) were covered by those included in the analysis (see paragraphs 10

and 11 above). The remaining less common transactions include: first party

transfers, bank initiated charges, unpaid and paid referral fees, branch bill

payments, CHAPS and unallocated transactions.

16. We received five transactional profiles from Barclays and four usable

transactional profiles from HSBC, RBS Group (RBSG), and Santander.

5

These can be found at Appendix B. Lloyds Banking Group (LBG) did not

submit any profiles as it did not believe that meaningful representative

customer profiles could be provided given SMEs’ diversity in cost to serve,

2

Business Moneyfacts presents BCA tariffs for around 130 different BCAs. Pricing data for Handelsbanken is not

available from the Business Moneyfacts website. We obtained its pricing data separately from Handelsbanken.

3

Barclays, HSBC, Lloyds Banking Group (LBG), RBS Group (RBSG) and Santander.

4

By transactional profile, we mean the number of transactions set out above that a representative customer

would make.

5

Of HSBC’s five profiles, one was simply the aggregate of the other four. In the case of RBSG and Santander,

we excluded one profile as it related to SMEs with turnover in excess of £2 million.

5

risk, average and range of balances, transaction volumes, channel preference

and need for relationship support.

6

17. Table 1 below shows an illustrative set of transactional profiles.

Table 1: An illustrative set of transactional profiles

Transaction

Weighting

50%

20%

15%

10%

5%

Description

£0–150k

£150–500k

light branch

user

£1500–500k

heavy

branch user

£500k–2m

light

branch

user

£500k–2m

heavy

branch

user

Profile

Profile 1

Profile 2

Profile 3

Profile 4

Profile 5

Electronic

Auto credit

1

6

2

15

5

Bill payment

0

0

0

0

0

Debit card

2

7

3

6

4

Direct debit

1

2

1

3

5

Standing order

0

6

1

15

1

Branch/other

Branch paying-in

0

0

5

2

8

Branch withdrawal

0

0

0

0

1

Branch cash-in

£20

£70

£1,520

£315

£4,300

Branch cash-out

£20

£30

£275

£50

£470

ATM cash-out

£15

£55

£130

£65

£70

Cheques paid-in

0

1

5

1

11

Cheques issued

1

1

3

2

8

Source: CMA analysis.

Methodology

18. For each profile, we calculated the monthly cost for each relevant tariff of

each bank by multiplying the number of transactions by the price per

transaction. Where monetary values were submitted, such as on cash

deposited and withdrawn, we divided the amount by 100 and rounded it up to

the nearest whole number to account for parts of £100 deposited or

withdrawn. We then multiplied this number by the fee applied to each £100

deposited/withdrawn.

19. Banks may have more than one relevant tariff, for example one tariff aimed at

SMEs with mainly electronic transactions and one aimed at those with more

branch transactions. Where this was the case, we took the tariff with the

lowest monthly cost overall. This assumes that SMEs choose the cheapest

tariff available for their pattern of transactions

7

. While this may not be true in

6

LBG considered that we should carry out analysis for BCAs using transactions data, similar to that for PCAs

(see paragraphs 30 to 34 below). However, as noted in the UIS Appendix C (paragraph 14), in contrast to PCAs

we did not already have transactions data and we considered the costs of obtaining such data would not be

proportionate to the potential benefits, given also that we had obtained representative profiles together with

weightings from four banks.

7

One bank ([]) stated that it ‘reviews each customer’s price plan on an annual basis. Where it considers that a

customer will be better off on a different payments plan, it will notify the customer and move them onto that price

plan.’

6

every case, we considered it more plausible than alternative assumptions, for

example assuming that SMEs choose at random (ie taking a simple average

across relevant tariffs).

20. When banks submitted their transactional profiles, in some cases they

specified the SME turnover band to which each profile related.

8

Banks’ tariffs

also sometimes have a turnover restriction (for example, the January 2015

TSB tariffs apply to SMEs with a maximum turnover of £0.5 million

9

). We only

included tariffs which applied within the turnover band of the profile.

10

21. Barclays offers discounts on monthly charges according to the length of time

its customers have been with Barclays. These discounts range from 5 to 30%

and depend on the customer’s turnover and on the length of its relationship

with Barclays. We calculated the weighted average discount rate for each

profile and applied it to Barclays’ monthly prices.

11

22. We then calculated a weighted average monthly BCA price for each bank and

banking group by applying the weightings to the profiles.

12

Results

23. As shown in Table 2, there is significant variation between banks’ charges.

The variation in monthly charges across banks is illustrated for one set of

profiles in Appendix C.

8

See Appendix B.

9

TSB now opens accounts for businesses with turnovers up to £2 million

10

As the TSB tariffs had a maximum turnover of £0.5 million, this meant we could not calculate a TSB price for

profiles applying to SMEs with turnover above £0.5 million. As a consequence, TSB was excluded from some

results.

11

We weighted discount rates in each turnover and tenure category by the number of customers in this category.

12

We calculated a weighted average price for LBG and RBSG using the proportion of these groups’ active BCAs

in Scotland (from these groups’ responses to the market questionnaire) as a proxy for the number of accounts at

Bank of Scotland and RBS respectively.

7

Table 2: Variation between lowest and highest monthly cost (highest as % of lowest monthly

cost)

%

Profiles

Barclays

HSBC

RBS

Santander

Great Britain

Profile 1

256.8

221.2

273.7

210.0

Profile 2

248.2

358.4

237.3

404.3

Profile 3

267.5

266.2

335.2

189.6

Profile 4

308.3

201.7

251.2

173.2

Profile 5

366.8

n/a

n/a

n/a

Northern Ireland

Profile 1

164.2

262.3

215.9

131.8

Profile 2

282.6

329.4

272.9

401.4

Profile 3

308.0

258.7

341.6

166.6

Profile 4

334.6

137.9

149.6

137.8

Profile 5

357.4

n/a

n/a

n/a

Source: CMA analysis.

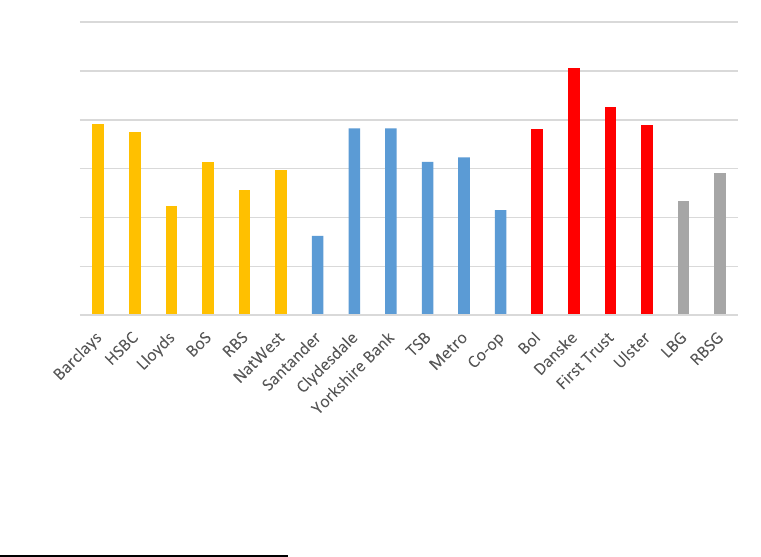

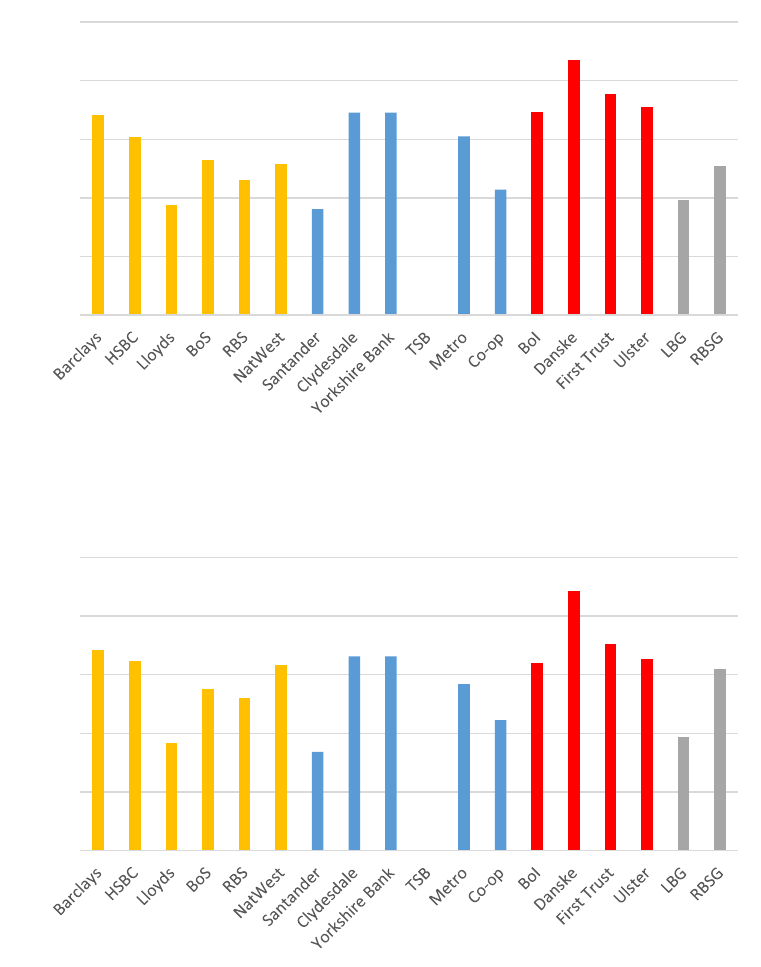

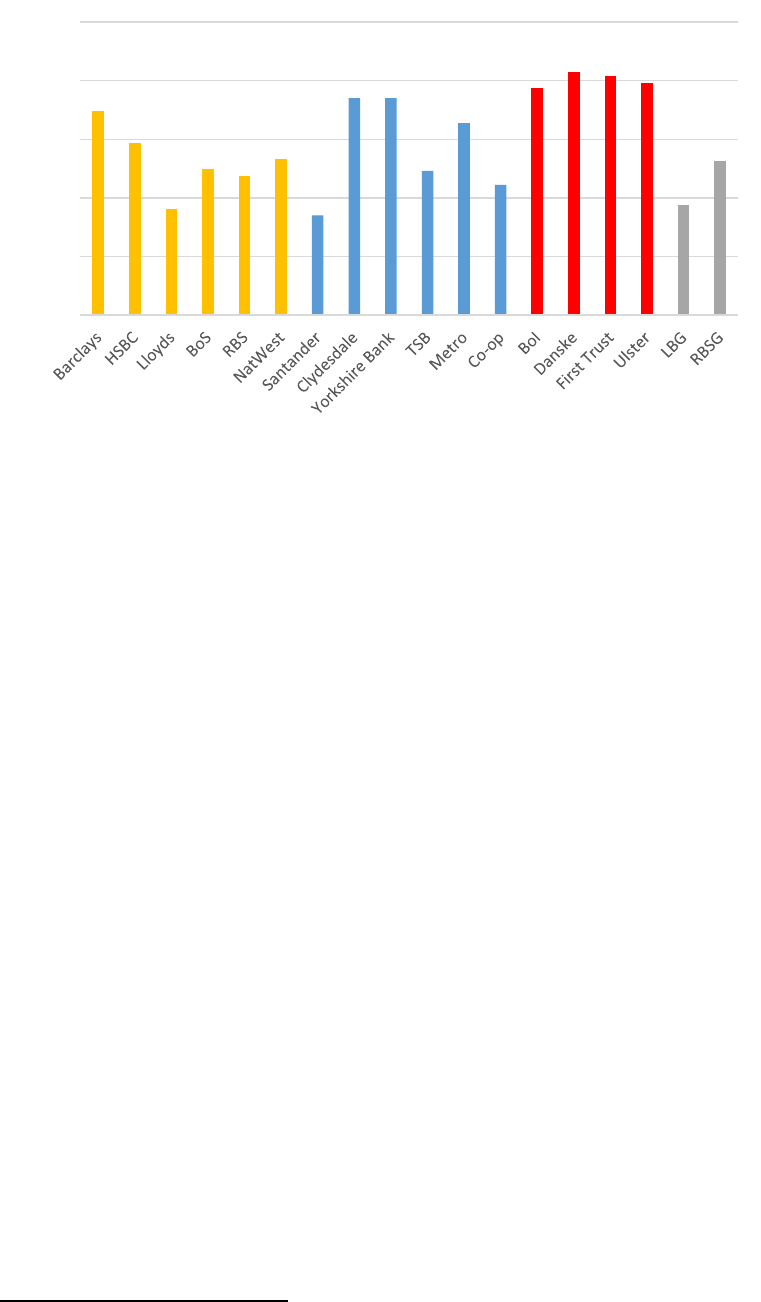

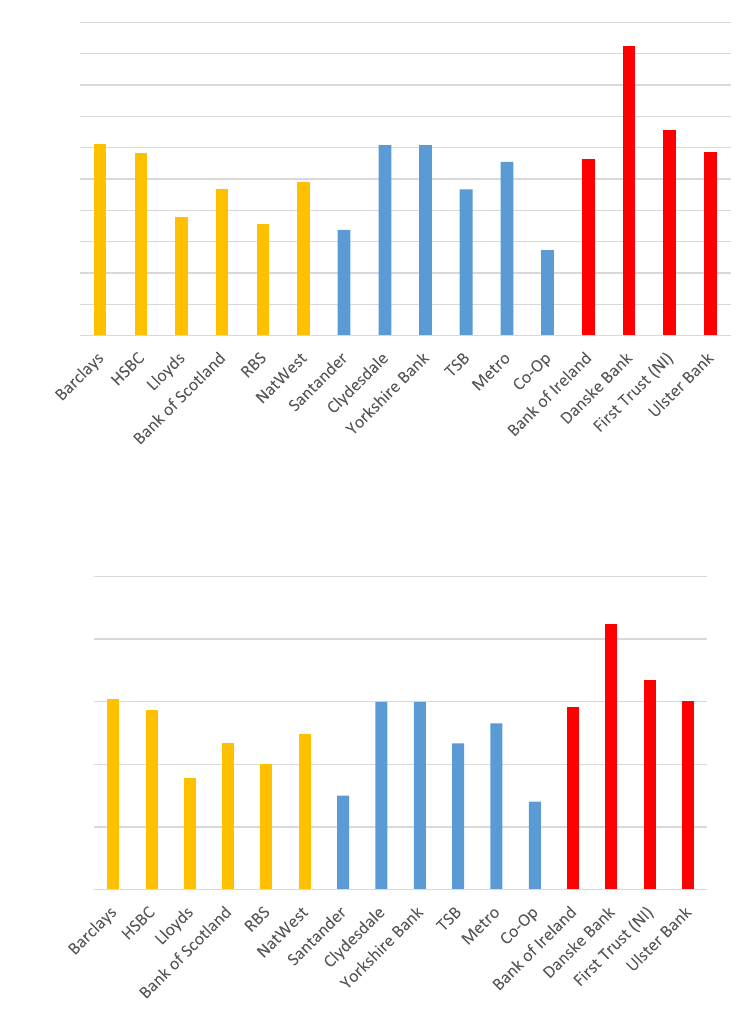

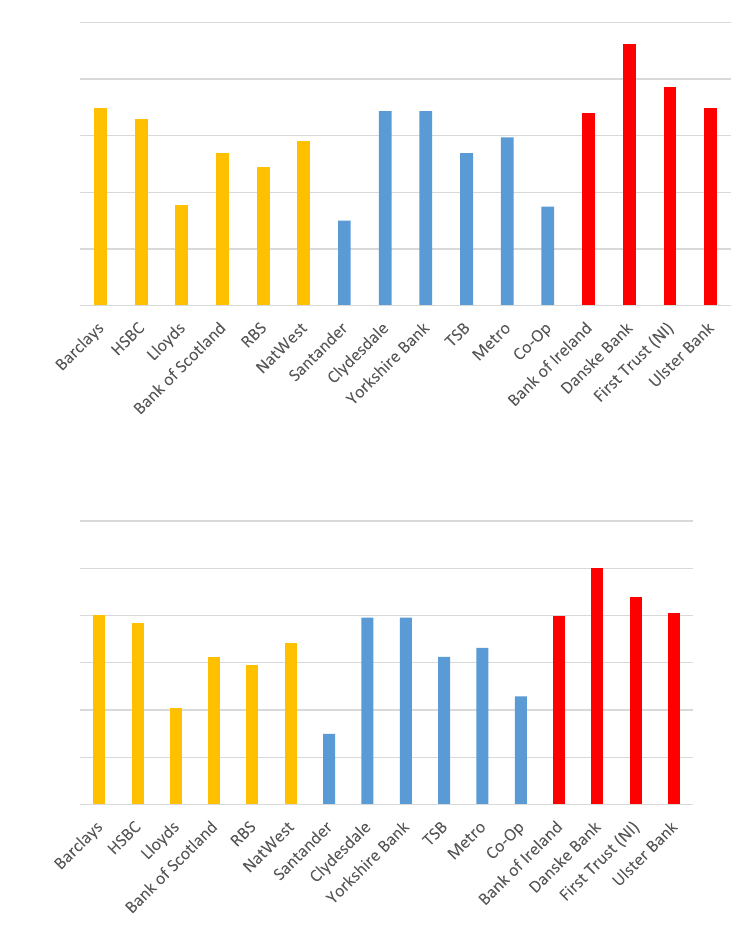

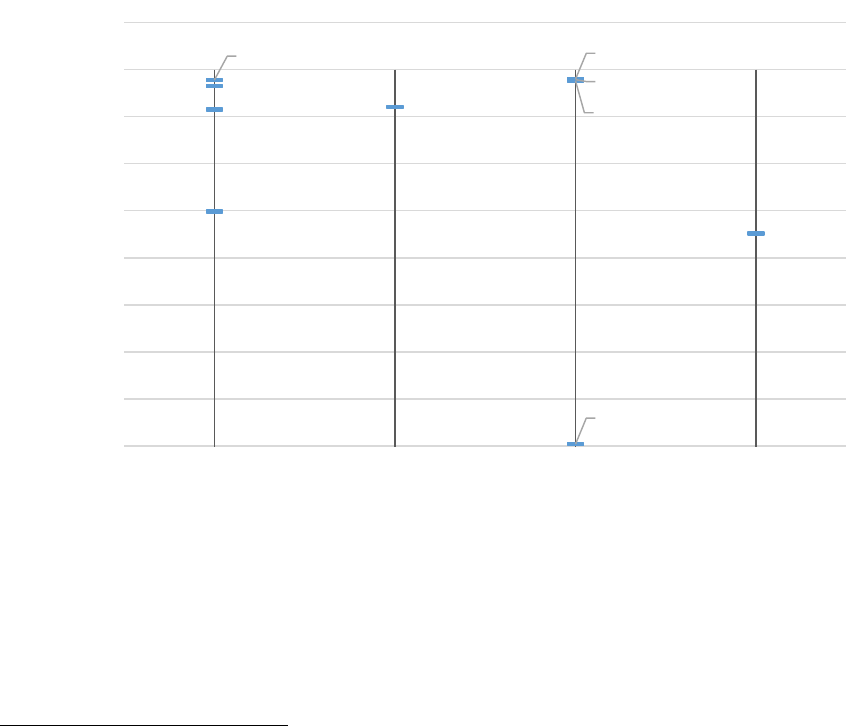

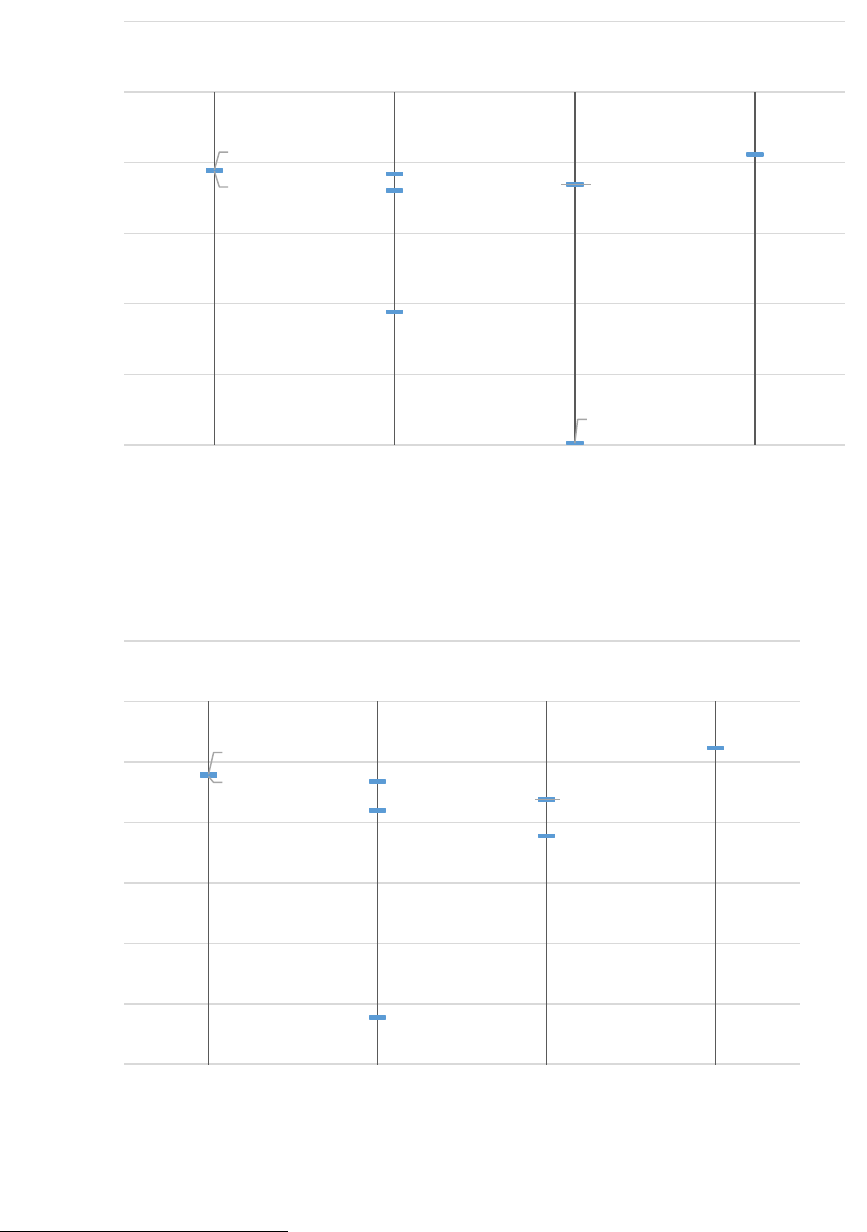

24. Figures 1 to 4 below show each bank’s weighted average prices calculated by

weighting the individual profiles. Four banks provided profiles; hence, there

are four sets of profiles and four sets of results.

13

Figure 1: Weighted average prices by bank based on Barclays profiles

Source: CMA analysis.

13

Yellow bars show larger banks, blue bars show smaller banks, red bars show Northern Ireland banks and grey

bars show weighted averages for the two banking groups whose constituent banks have different weighted

average prices. TSB is excluded from some results since we were not able to calculate a weighted average price

for TSB where at least one profile related to SMEs with turnover in excess of £500,000.

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£30.00

8

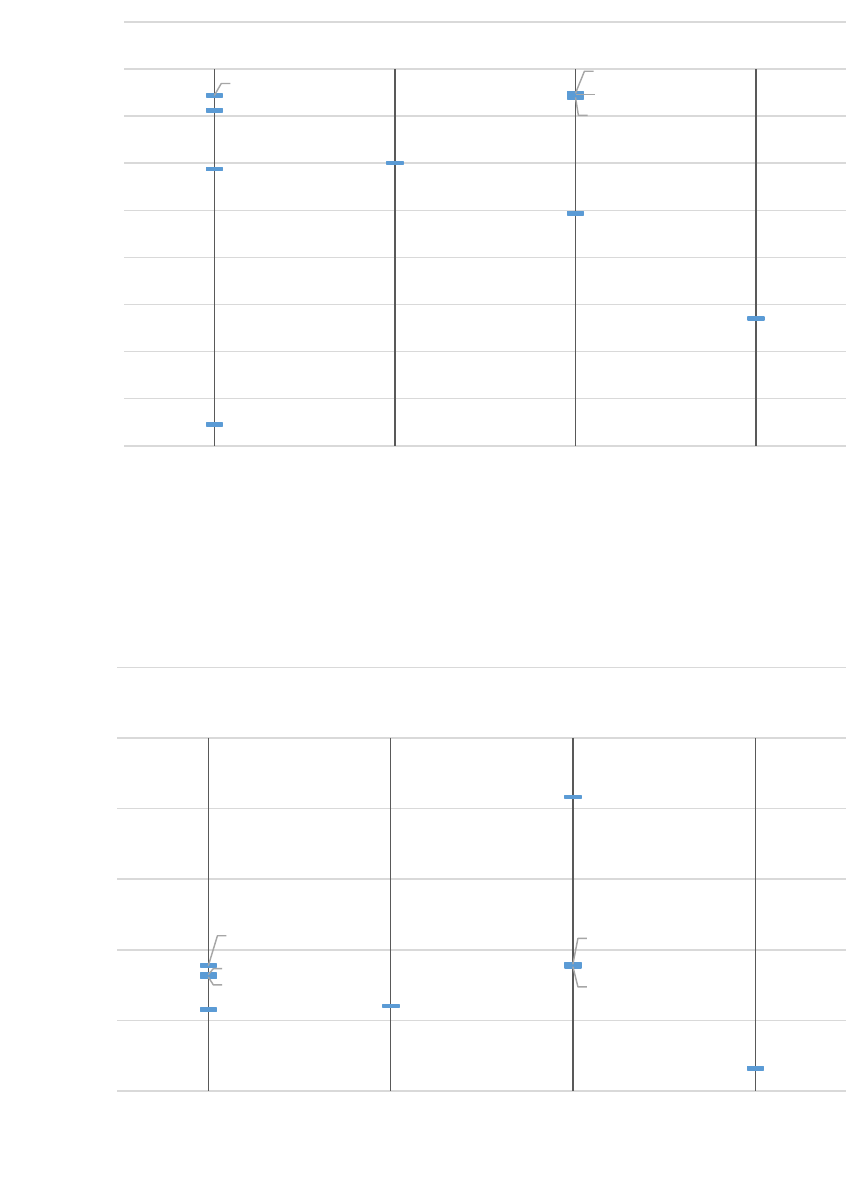

Figure 2: Weighted average prices by bank based on HSBC profiles

Source: CMA analysis.

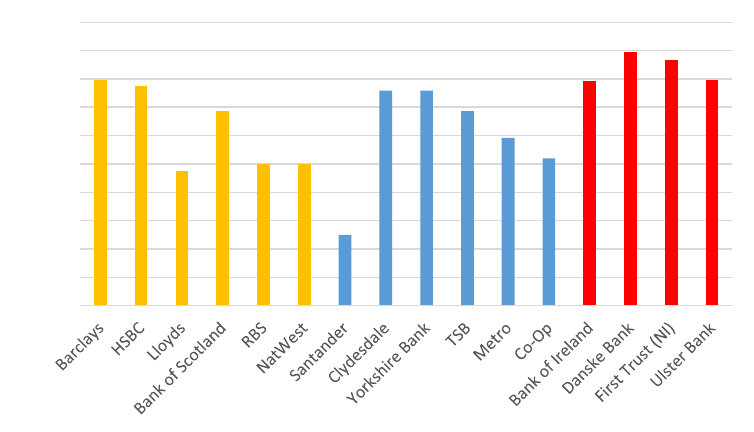

Figure 3: Weighted average prices by bank based on RBS profiles

Source: CMA analysis.

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

9

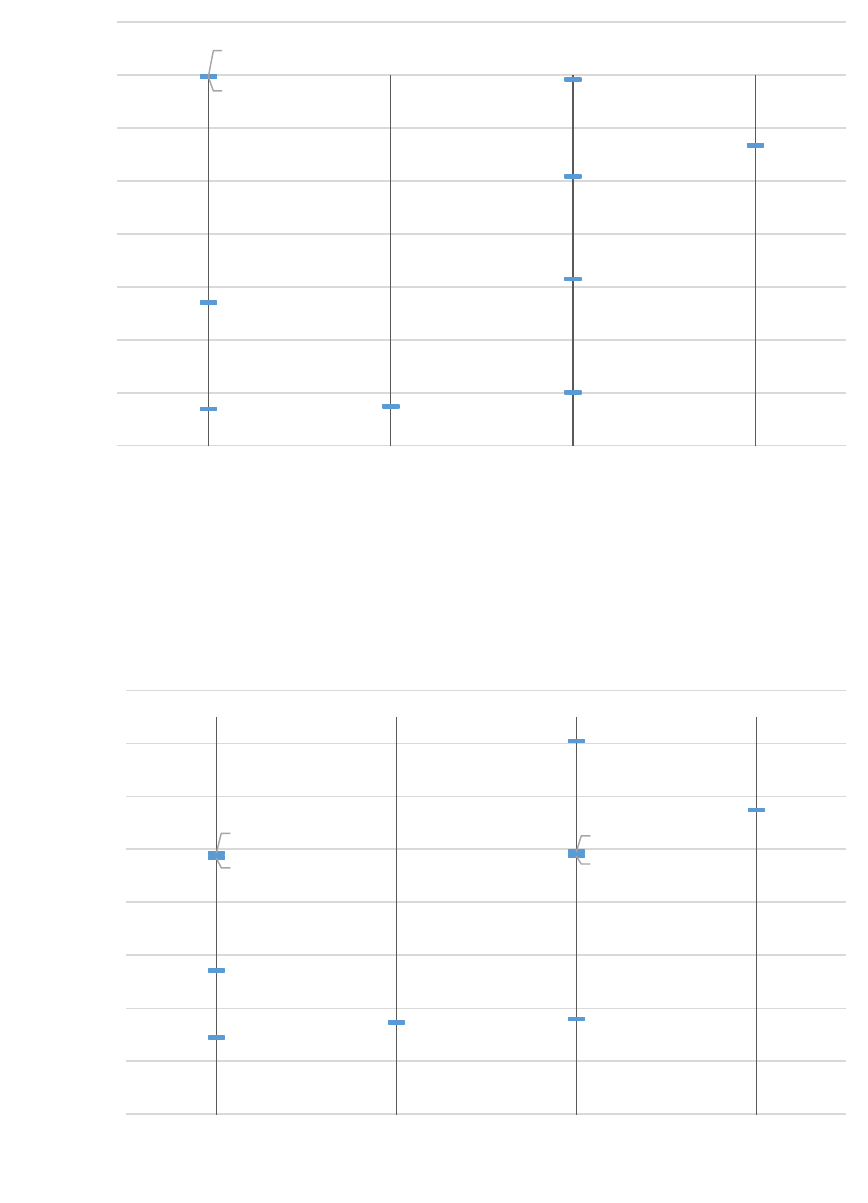

Figure 4: Weighted average prices by bank based on Santander profiles

Source: CMA analysis.

25. We note that the relative prices are broadly similar for all four sets of results.

26. Handelsbanken was not included in the above analysis as its prices are not

published. Handelsbanken provided us with its guide prices and we used

these to calculate indicative weighted average prices on a similar basis to the

other banks. Based on these guide prices, Handelsbanken’s prices are above

those of the other banks.

14

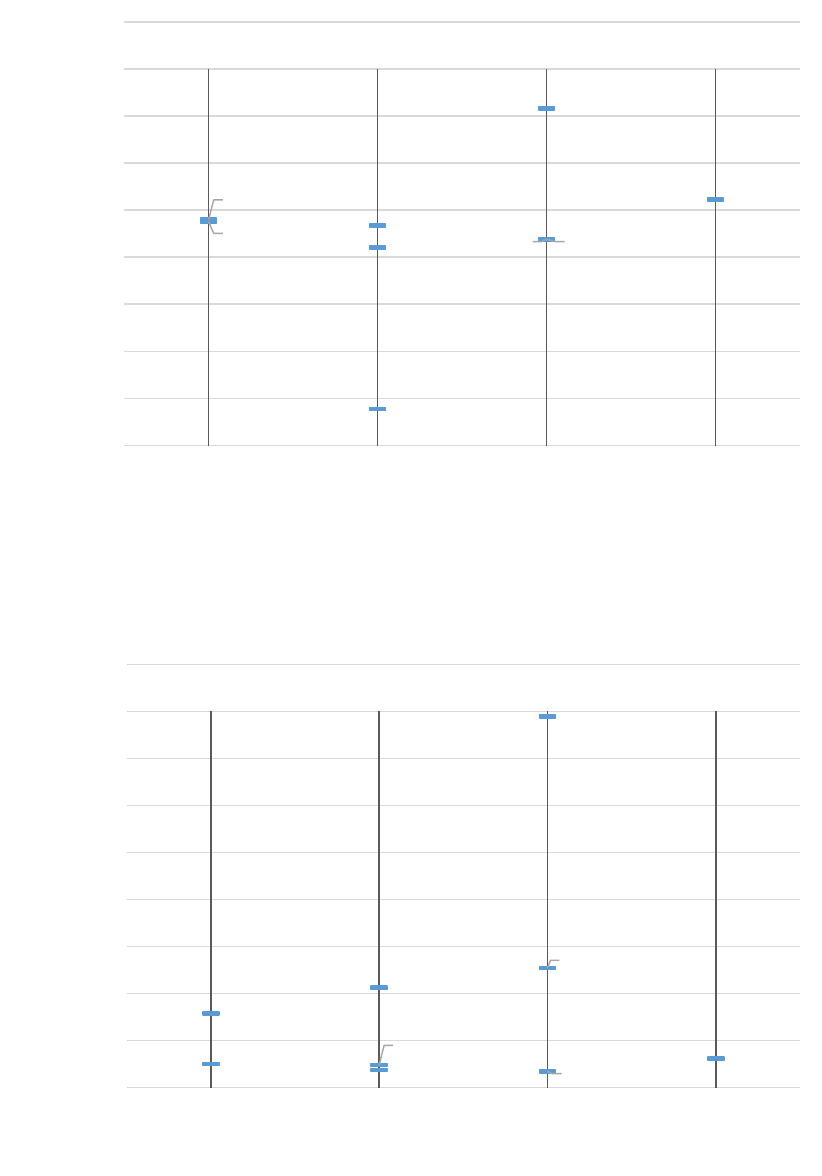

27. As set out in the UIS, one of the questions we are addressing with our pricing

analysis is whether banks with a higher market share tend to charge higher

prices than smaller banks.

15

Figures 5–8 below show the weighted average

price against market share in Great Britain (market shares are shown in

ranges as a number of parties said their market shares were confidential).

These do not show any clear association between price and market share,

though Santander’s prices are consistently amongst the lowest. Appendix D

shows weighted average price against market share in NI and these similarly

do not show any clear association between price and market share.

14

This reflects in particular Handelsbanken’s indicative monthly charge of £50, but this is a guide price only and

its branch managers can set their own prices for bespoke products and services.

15

See UIS, Appendix C paragraph 3.

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

10

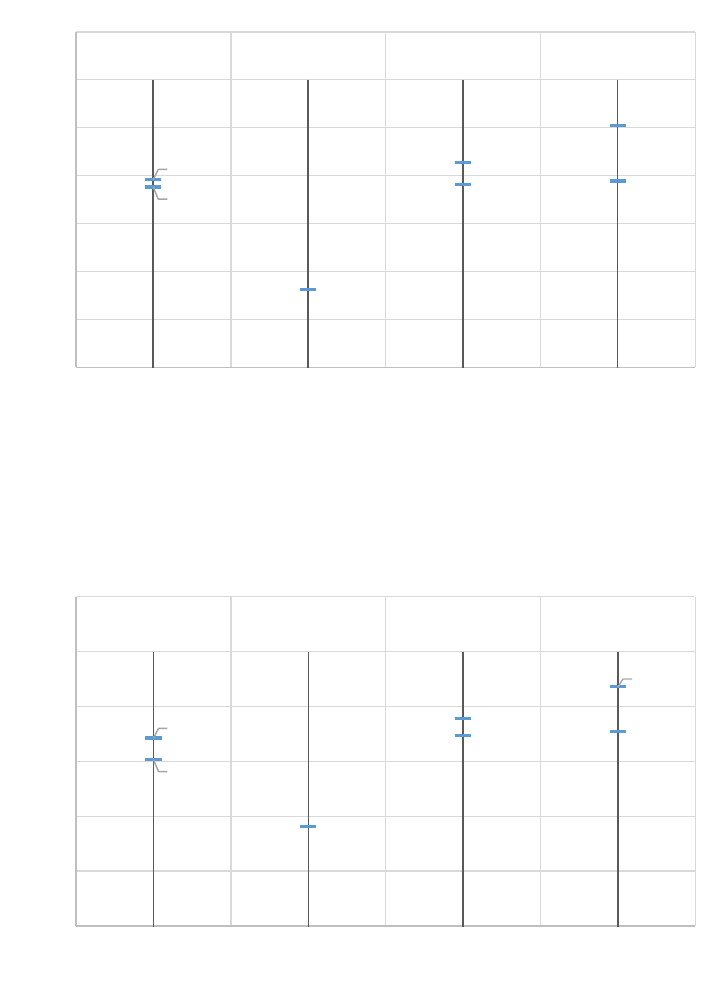

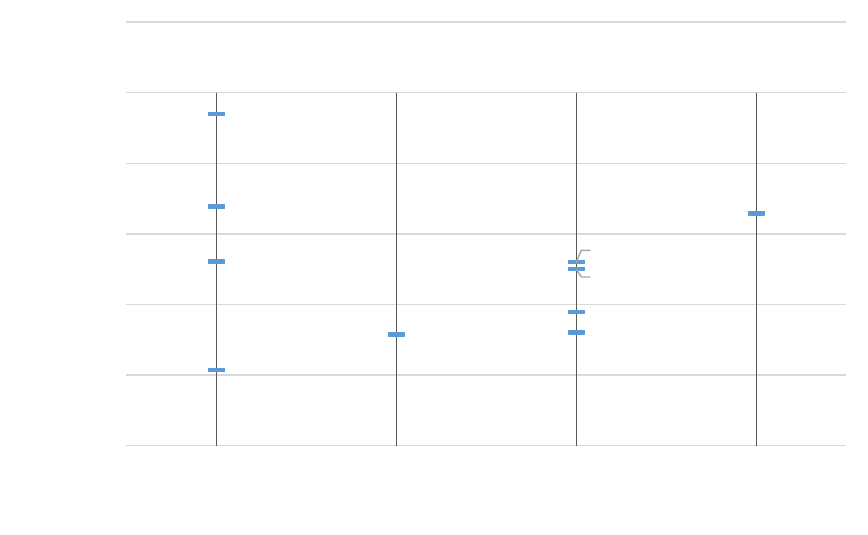

Figure 5: Weighted average monthly BCA price in GB, based on the profiles submitted by

Barclays

Source: CMA analysis.

Figure 6: Weighted average monthly BCA price in GB, based on the profiles submitted by

HSBC

Source: CMA analysis.

Barclays

HSBC

LBG

RBSG

Santander

Clydesdale

TSB

Metro

Co-op

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Barclays

HSBC

LBG

RBSG

Santander

Clydesdale

Metro

Co-op

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

11

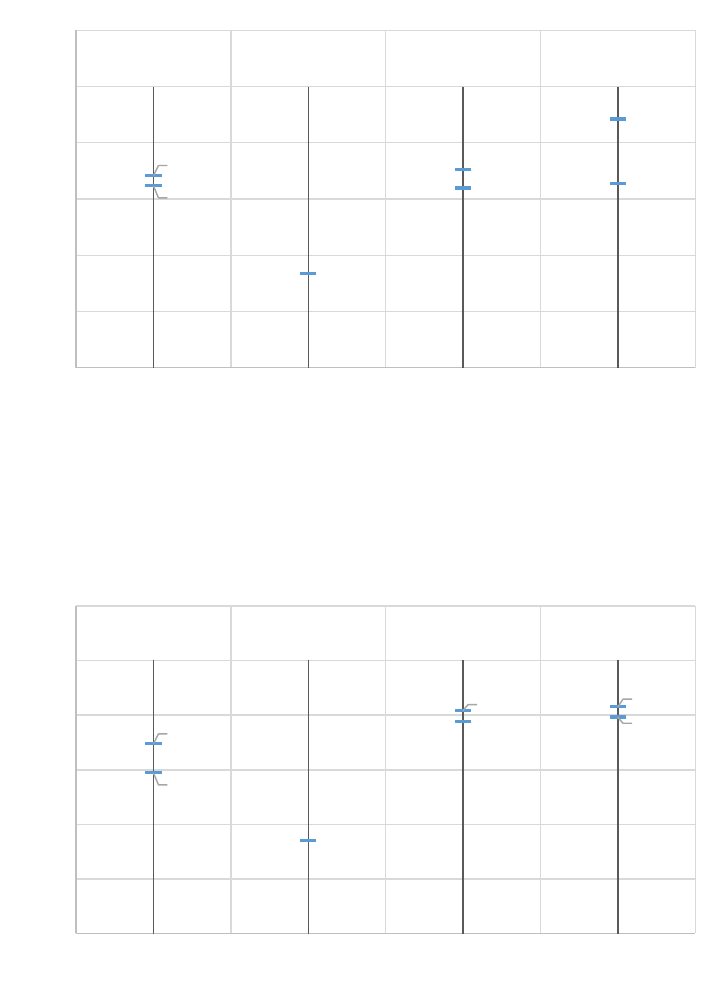

Figure 7: Weighted average monthly BCA price in GB, based on the profiles submitted by RBS

Source: CMA analysis.

Figure 8: Weighted average monthly BCA price in GB, based on the profiles submitted by

Santander

Source: CMA analysis.

Interpretation of the analysis

28. As discussed in the UIS Appendix C,

16

any comparison of prices needs to be

interpreted with caution for a number of reasons. These include:

(a) There are limitations in the coverage of the analysis, in particular it does

not take into account differences in credit balances, overdrafts and

16

See paragraph 22.

Barclays

HSBC

LBG

RBSG

Santander

Clydesdale

Metro

Co-op

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Barclays

HSBC

LBG

RBSG

Santander

Clydesdale

Metro

Co-op

TSB

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

12

incentives (see Appendix A). It is also limited to SMEs under £2 million

turnover.

(b) The analysis is based on a small number of profiles and may not be fully

reflective of all SMEs. As noted by RBS in its response to the UIS, SMEs

are a diverse customer group and designing representative user profiles

is a particularly difficult challenge.

17

The analysis is also based on the

assumption that SMEs are on the lowest priced available tariff (see

paragraph 19). It also does not take account of any negotiation of prices

(though this is less prevalent for SMEs under £2 million turnover).

(c) Differences in prices may reflect quality of service differences. RBS said

that the relationship and service components were typically more valued

by SME customers and the particular service given to SMEs was tailored

to the particular needs of the business, which will be determined by its

size, the sector in which it is active and the nature of the SME

business.

18

Similarly, Barclays said that any pricing analysis needed to

also take into account differences in quality of service.

19

As noted in the

UIS, we are looking separately at data on quality of service, and

differences in quality of service will need to be borne in mind when

considering any price differences. We do not consider that the value to

consumers of quality of service differences can be calculated with

sufficient accuracy to calculate prices adjusted for quality of service.

Therefore, the results of pricing and quality of service comparisons will

need to be considered together.

29. Any differences in average prices between providers may have a number of

explanations, including growth strategy (an expanding bank may have lower

prices because it has more active and fewer inactive customers) and balance

sheet strategy.

Personal current accounts (PCAs)

30. We set out the results of our initial comparison of PCA prices based on six

illustrative profiles in the UIS (see Appendix C, Annex 2): figures C1 to C12

showed weighted average price against market share. These figures were

excised from the published version of the UIS as a number of parties said

their market shares were confidential. Appendix E shows revised versions of

these figures using ranges for market shares.

17

RBS response to UIS, section 3.1.3.

18

RBS response to UIS, section 3.2.2 ii) b).

19

Barclays response to UIS, paragraph 4.5.4.

13

31. We stated in the UIS that we intended to extend this analysis using

transactions data for a representative, large sample of PCA customers.

32. We issued a consultation paper on how we proposed to do this on 23 June

2015.

20

This set out how we intended to carry out the analysis using

transactions data and explained that we intended to contract the calculation of

monthly PCA costs to Runpath Digital Ltd (Runpath).

33. In response to this consultation, a number of parties supported this further

analysis as it was likely to provide more robust results than our initial analysis

based on six illustrative profiles. One Northern Ireland bank ([]) said it

believed that we would not be able to draw any reliable conclusions because

of limitations in the transactions data. We acknowledge there are limitations in

the data for some Northern Ireland banks and that this may affect the

robustness of comparisons which include customers of the Northern Ireland

banks; however, it would not affect comparisons for customers in Great

Britain. We stated in the UIS and the consultation that price comparisons

need to be interpreted together with quality comparisons,

21

and this point was

emphasised by some parties. We will include our comparisons of quality

indicators with our provisional findings report.

34. We considered that we should proceed with the analysis using transactions

data and we have now issued the contract to Runpath. We are considering

with Runpath the detailed suggestions made by parties in response to the

consultation. The results of the analysis will be included in our provisional

findings.

20

PCA pricing analysis using transactions data.

21

See UIS Appendix C paragraph 22 and consultation on PCA pricing using transactions data, paragraph 24.

14

Appendix A: BCA credit interest rates, overdraft charges and

customer incentives

Interest rates on credit balances

1. As noted in paragraph 7 of the main working paper, some banks offer interest

on credit balances. 8 out of 32 tariffs used in our analysis offer interest on in-

credit balances. The interest rate (AER) for these 8 tariffs varied from 0.05%

to 0.25%, see Table 1 below. We were not able to include interest on credit

balances in our weighted average prices as we did not have average credit

balances for the profiles obtained from the four banks.

22

Table 1: Interest rates offered on credit balances

%

Bank

Tariff

Balances

< £999

Balances

£1,000–

£4,999

Balances

£5,000–

£9,999

Balances

£10,000–

£24,999

Balances

£25,000–

£99,999

Balances

£100,000–

£249,999

Balances

>£250,00

0

RBS

Business Plus

0.05

0.05

0.05

0.05

0.05

0.05

0.05

RBS

Royalties

0.05

0.05

0.05

0.05

0.05

0.05

0.05

NatWest

Business Plus

0.05

0.05

0.05

0.05

0.05

0.05

0.05

NatWest

Advantage

0.05

0.05

0.05

0.05

0.05

0.05

0.05

Santander

Business Current

0.25

0.25

0.25

0.25

0.25

0.25

0.25

Santander

Corporate Current

0.10

0.10

0.10

0.10

0.10

0.10

0.10

Santander

Corporate Current +

0.15

0.15

0.15

0.15

0.15

0.15

0.15

Co-op*

Business Direct Plus

0

0.12

0.15

0.18

0.21

0.25

0.28

Source: Business Moneyfacts

* New rates and tiers were introduced in July 2015

22

Metro Bank does not pay interest on credit balances but offers a reduction in fees for accounts with a balance

which stays above £5,000 for the whole month. For accounts which meet this condition, the monthly fee is

waived and they are entitled to 50 free day to day transactions. As we do not have credit balances, this waiver

has been excluded from our calculations.

15

Overdrafts

2. BCAs may include a facility to apply for arranged overdrafts and this is a

significant source of revenue for banks,

23

though survey evidence suggests

only around 15% of SMEs have overdrafts.

24

As with PCAs, banks may allow

SMEs to make payments even when this would take them beyond their

borrowing limit, but such unauthorised overdrafts are a less important source

of revenue for BCAs than PCAs.

25

3. Table 2 shows published prices on overdrafts from Business Moneyfacts.

4. We were not able to include overdrafts in our weighted average prices as

published prices for arranged overdrafts are in many cases unavailable (see

Table 2).

23

See UIS, Appendix C, Annex 4.

24

BDRC/BIS SME Finance Monitor.

25

See UIS, Appendix C, Annex 4.

16

Table 2: Overdraft charges

Authorised

Unauthorised

%pm

%*

Arrangement

fee

%pm

%*

Extra fee

Barclays

Negotiable

Negotiable

Negotiable

n/a

29.5%

Negotiable

HSBC

Negotiable

Negotiable

Tiered/varies

1.63%

21.34%

£4 per working day debit

balance is over existing

formally arranged

overdraft or £8 per

working day account is

overdrawn with no

formally arranged

overdraft limit in place

LBG†

0.88%

10.56%

Negotiable

2.20%

26.4%

£15 per day if overdraft

increases by £50 or more

RBS/NatWest

Negotiable

Negotiable

Tiered/varies

n/a

29.5% APR**

£30 per day capped at

£120 per month

Santander

n/a

5% ABR§

1% (subject

to minimum

charge of

£50)

n/a

25% ABR§

Nil

Clydesdale

Negotiable

Negotiable

Negotiable

n/a

33.51%

£25 per day

TSB

0.88%

10.56%

1.5% (Min

£100)

2.20%

26.4%

£15 per day if overdraft

increases by £50 or more

Metro‡

0.80%

10%

1.75% (Min

£50)

1.88%

25%

Nil

Co-op#

Negotiable

Negotiable

Negotiable

1.92%

25.6%

£20 per day if overdraft

increases or £20 per

month if overdraft occurs

Bank of

Ireland

Negotiable

Negotiable

Tiered/varies

Negotiable

Negotiable

Nil

Danske

Negotiable

Negotiable

Negotiable

Negotiable

Negotiable

Nil

First Trust

Negotiable

Negotiable

Tiered/varies

1.50%

(subject to

a minimum

charge of

£2/month)

Base rate

plus 12%

Nil

Ulster

Negotiable

Negotiable

Negotiable

n/a

17%

Nil

Source: Business Moneyfacts.

* Effective Annual Rate unless otherwise specified.

† Rates are for Tracker overdrafts. Base rate overdrafts are individually negotiated and are typically below the Tracker

overdraft rate.

** Annual Percentage Rate

§ Above Base Rate

‡ Rates are for overdraft with a limit of up to £25,000. For amounts over £25,000, a fixed or variable margin over the Metro

Bank Base Rate (currently 0.50%) and an arrangement fee of 1.25% of the limit.

#These are the overdraft terms for the Co-op’s standard current account, not those of Co-op’s other BCAs such as Business

Direct.

Incentives offered to new customers

5. As illustrated in Table 3 below, banks typically offer incentives to new

customers. The impact of such incentives on the average price paid by SMEs

depends on how long the customer continues to hold the account with the

17

bank concerned. We have not included such incentives in this analysis. We

noted that, in principle, this could be done by calculating total cost over

different periods of holding a BCA (eg two years, five years, ten years) but we

considered it would make the analysis excessively complex.

Table 3: BCA incentives offered by banks to startups and switchers, January 2015

Bank

BCA incentives

Startups* (period with no

monthly/ standard transaction

charges)

Switchers (period with no monthly/

standard transaction charges or

cash payment)

Barclays

12 months

†

HSBC

18 months‡

6 months**

Lloyds

18 months§

6 months§

Bank of Scotland

18 months

6 months

RBS, NatWest

24 months#

£150–£250##

Santander

12 months¶

Clydesdale

24 months§§

18 months§§

Yorkshire Bank

24 months§§

18 months§§

TSB

18 months

6 months~

Metro

Co-op

Special offer to members of Federation of Small Businesses††

Bank of Ireland

No transaction charges for 12

months and a 50% discount for

a further 12 months$

‡‡

Danske Bank

12 months~~

6 months***

First Trust

For those with certain loan types, 12 months free banking

Ulster Bank

24 months

Source: Banks’ responses to Question 11 in SME MQ (January 2015), supplemented by bank websites.

* Typically businesses in first year of business, setting up their first BCA.

† []

‡ £2 million turnover or below (startups with annual turnover above £2 million are offered bespoke terms that are negotiated

with their relationship manager and may include a period of free banking).

** Turnover up to £0.5 million (now increased to 12 months). Switchers with turnover of £0.5 million to £2 million may be offered

a period of free banking following a discussion with their relationship manager and those with annual turnover above £2 million

are offered bespoke terms that are negotiated with their relationship manager and may include a period of free banking.

§ Also offers fee-free overdrafts.

# Up to £1 million turnover. Also offers a fee free overdraft facility of £500 for the first 12 months.

## For customers with turnover of up to £2 million, accounts are credited £150 (or £250 if the customer also switches an

overdraft) by the end of the fourth full month after account opening.

¶ Additional six months if customer has PCA with Santander, or switches to it.

§§ Increase to 25 months for startups and switchers with effect from 4 May 2015.

~ Changed from 6 to 18 months effective from 15 June 2015.

†† Co-op offers FSB Business Banking Account customers free banking, £25 annual loyalty reward and a fee free overdraft.

$ Except for cash deposits greater than £10,000 per quarter.

‡‡ No free banking offer for switchers, but a three year package for growing businesses.

~~ Extended to 24 months if the business owners/directors have/switch to a PCA with Danske.

*** Extended to 12 months if the business owners/directors have/switch to a PCA with Danske. Also offers 12 months free

Business e-Banking (payments module) and no arrangement fees on certain products during the first 12 months.

18

Appendix B: BCA customer profiles

Table 1: Barclays transactional profiles

Transaction

Weighting

[]

[]

[]

[]

[]

Description

[]

[]

[]

[]

[]

Profile

[]

[]

[]

[]

[]

Electronic

Auto credit

[]

[]

[]

[]

[]

Bill payment

[]

[]

[]

[]

[]

Debit card

[]

[]

[]

[]

[]

Direct debit

[]

[]

[]

[]

[]

Standing order

[]

[]

[]

[]

[]

Branch/other

Branch paying-in

[]

[]

[]

[]

[]

Branch withdrawal

[]

[]

[]

[]

[]

Branch cash-in

[]

[]

[]

[]

[]

Branch cash-out

[]

[]

[]

[]

[]

ATM cash-out

[]

[]

[]

[]

[]

Cheques paid-in

[]

[]

[]

[]

[]

Cheques issued

[]

[]

[]

[]

[]

Source: Barclays.

* []

Table 2: HSBC transactional profiles

Transaction

Weighting

[]

[]

[]

[]

Description

[]

[]

[]

[]

Profile

[]

[]

[]

[]

Electronic

Auto credit

[]

[]

[]

[]

Bill payment

[]

[]

[]

[]

Debit card

[]

[]

[]

[]

Direct debit

[]

[]

[]

[]

Standing order

[]

[]

[]

[]

Branch/other

Branch Paying in

[]

[]

[]

[]

Branch Withdrawal

[]

[]

[]

[]

Branch Cash In

[]

[]

[]

[]

Branch Cash Out

[]

[]

[]

[]

ATM Cash Out

[]

[]

[]

[]

Cheques Paid In

[]

[]

[]

[]

Cheques Issued

[]

[]

[]

[]

Source: HSBC.

19

Table 3: RBS/NatWest transactional profiles*

Transaction

Weighting

[]

[]

[]

[]

Description

[]

[]

[]

[]

Profile

[]

[]

[]

[]

Electronic

Auto credit (includes BIB BACS)

[]

[]

[]

[]

Bill payment

[]

[]

[]

[]

Debit card/Other auto debits

[]

[]

[]

[]

Direct debit

[]

[]

[]

[]

Standing order

[]

[]

[]

[]

Branch/other

Branch paying-in

[]

[]

[]

[]

Branch withdrawal

[]

[]

[]

[]

Branch cash-in

[]

[]

[]

[]

Branch cash-out

[]

[]

[]

[]

ATM cash-out‡

[]

[]

[]

[]

Cheques paid-in

[]

[]

[]

[]

Cheques issued

[]

[]

[]

[]

Source: RBS.

* The figures refer to the median (50

th

percentile) usage of each transaction type by SMEs falling within each turnover band.

‡ []

Table 4: Santander transactional profiles

Transaction

Weighting

[]

[]

[]

[]

Description

[]

[]

[]

[]

Profile

[]

[]

[]

[]

Electronic

Auto credit

[]

[]

[]

[]

Bill payment

[]

[]

[]

[]

Debit card

[]

[]

[]

[]

Direct debit

[]

[]

[]

[]

Standing order

[]

[]

[]

[]

Branch/other

Branch paying-in

[]

[]

[]

[]

Branch withdrawal

[]

[]

[]

[]

Branch cash-in

[]

[]

[]

[]

Branch cash-out

[]

[]

[]

[]

ATM cash-out

[]

[]

[]

[]

Cheques paid-in

[]

[]

[]

[]

Cheques issued

[]

[]

[]

[]

Source: Santander.

20

Appendix C: Figures by profile for the BCA monthly charge

The figures below are based on the profiles submitted by Barclays.

Profile 1

Profile 2

£0.00

£2.00

£4.00

£6.00

£8.00

£10.00

£12.00

£14.00

£16.00

£18.00

£20.00

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

21

Profile 3

Profile 4

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£30.00

22

Profile 5

Source: CMA analysis.

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£30.00

£35.00

£40.00

£45.00

£50.00

23

Appendix D: Weighted average BCA price in Northern Ireland

Figure 1: Weighted average monthly BCA price in Northern Ireland, based on the profiles

submitted by Barclays

Source: CMA analysis.

Figure 2: Weighted average monthly BCA price in Northern Ireland, based on the profiles

submitted by HSBC

Source: CMA analysis.

BoI

Danske

First Trust (AIB)

Ulster

Barclays

HSBC

Santander

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£30.00

£35.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

BoI

Danske

First Trust (AIB)

Ulster

Barclays

HSBC

Santander

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£30.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

24

Figure 3: Weighted average monthly BCA price in Northern Ireland, based on the profiles

submitted by RBS

Source: CMA analysis.

Figure 4: Weighted average monthly BCA price in Northern Ireland, based on the profiles

submitted by Santander

Source: CMA analysis.

BoI

Danske

First Trust (AIB)

Ulster

Barclays

HSBC

Santander

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£30.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

BoI

Danske

First Trust (AIB)

Ulster

Barclays

HSBC

Santander

£0.00

£5.00

£10.00

£15.00

£20.00

£25.00

£30.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

25

Appendix E: PCA monthly price against market share

1. Figures 1 to 12 below compare each banking group’s average price for each

of the six profiles against its market share for Great Britain (Figures 1 to 6)

and Northern Ireland (Figures 7 to 12). These are the same as Figures C1 to

C12 in UIS Appendix C Annex 2 except that only the market share ranges are

shown.

2. As explained in UIS Appendix C, these results relate to the monthly cost for

each customer profile of standard and interest-paying or ‘reward’ PCAs.

26

The

monthly price for each banking group in the charts below is a weighted

average of these monthly costs where the weights are the number of active

accounts for each relevant PCA offered by that banking group.

Great Britain

Figure 1: Monthly GB prices for profile 1: no overdraft and average credit balance of £5,000

Source: CMA analysis.

26

Where a bank brand had more than one relevant PCA, we took the one with the largest number of active

accounts – an active PCA is defined as one which has at least one customer-generated payment or transfer

(including SO and DD, but excluding charges and interest on the account) coming into, or leaving, the account in

the previous 12 months.

Barclays

HSBCG

LBG

RBSG

Santander

Clydesdale

Nationwide

TSB

Co-op

Metro

(£3.00)

(£2.50)

(£2.00)

(£1.50)

(£1.00)

(£0.50)

£0.00

£0.50

£1.00

£1.50

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

26

Figure 2: Monthly GB prices for profile 2: no overdraft and average credit balance of £2,500

Source: CMA analysis.

Figure 3: Monthly GB prices for profile 3: no overdraft and average credit balance of £500

Source: CMA analysis.

Barclays

HSBCG

LBG

RBSG

Santander

Clydesdale

Nationwide

TSB

Co-op

Metro

(£0.60)

(£0.40)

(£0.20)

£0.00

£0.20

£0.40

£0.60

£0.80

£1.00

£1.20

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

Barclays

HSBCG

LBG

RBSG

Santander

Clydesdale

Nationwide

TSB

Co-op

Metro

£0.00

£0.50

£1.00

£1.50

£2.00

£2.50

£3.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

27

Figure 4: Monthly GB prices for profile 4: three consecutive days in arranged overdraft of £100

and average credit balance of £500 for the remainder of the month

Source: CMA analysis.

Figure 5: Monthly GB prices for profile 5: 12 consecutive days in arranged overdraft of £500

and average credit balance of £500 for the remainder of the month

Source: CMA analysis.

Barclays

HSBCG

LBG

RBSG

Santander

Clydesdale

Nationwide

TSB

Co-op

Metro

£0.00

£1.00

£2.00

£3.00

£4.00

£5.00

£6.00

£7.00

£8.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

Barclays

HSBCG

LBG

RBSG

Santander

Clydesdale

Nationwide

TSB

Co-op

Metro

£0.00

£2.00

£4.00

£6.00

£8.00

£10.00

£12.00

£14.00

£16.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

28

Figure 6: Monthly GB prices for profile 6: three consecutive days in unarranged overdraft of

£100 and average credit balance of £500 for the remainder of the month, and one unpaid item

totalling less than £50

Source: CMA analysis.

Barclays

HSBCG

LBG

RBSG

Santander

Clydesdale

Nationwide

TSB

Co-op

Metro

£0.00

£10.00

£20.00

£30.00

£40.00

£50.00

£60.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

29

Northern Ireland (NI)

27

Figure 7: Monthly NI prices for profile 1: no overdraft and average credit balance of £5,000

Source: CMA analysis.

Figure 8: Monthly NI prices for Profile 2: no overdraft and average credit balance of £2,500

Source: CMA analysis.

27

The charts show weighted average price for banks with a material number of accounts in Northern Ireland

against their market share in Northern Ireland.

DanskeAIB

Bank of Ireland

Ulster (RBS)

Barclays

HSBCG

Halifax (LBG)

Santander

Nationwide

(£3.00)

(£2.00)

(£1.00)

£0.00

£1.00

£2.00

£3.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

DanskeAIB

Bank of Ireland

Ulster (RBS)

Barclays

HSBCG

Halifax (LBG)

Santander

Nationwide

(£1.50)

(£1.00)

(£0.50)

£0.00

£0.50

£1.00

£1.50

£2.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

30

Figure 9: Monthly NI prices for profile 3: no overdraft and average credit balance of £500

Source: CMA analysis.

Figure 10: Monthly NI prices for profile 4: three consecutive days in arranged overdraft of £100

and average credit balance of £500 for the remainder of the month

Source: CMA analysis.

DanskeAIB

Bank of Ireland

Ulster (RBS)

Barclays

HSBCG

Halifax (LBG)

Santander

Nationwide

(£1.50)

(£1.00)

(£0.50)

£0.00

£0.50

£1.00

£1.50

£2.00

£2.50

£3.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

Danske

AIB

Bank of Ireland

Ulster (RBS)

Barclays

HSBCG

Halifax (LBG)

Santander

Nationwide

£0.00

£2.00

£4.00

£6.00

£8.00

£10.00

£12.00

£14.00

£16.00

£18.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

31

Figure 11: Monthly NI prices for profile 5: 12 consecutive days in arranged overdraft of £500

and average credit balance of £500 for the remainder of the month

Source: CMA analysis.

Figure 12: Monthly NI prices for profile 6: three consecutive days in unarranged overdraft of

£100 and average credit balance of £500 for the remainder of the month, and one unpaid item

totalling less than £50

Source: CMA analysis.

Danske

AIB

Bank of Ireland

Ulster (RBS)

Barclays

HSBCG

Halifax (LBG)

Santander

Nationwide

£0.00

£2.00

£4.00

£6.00

£8.00

£10.00

£12.00

£14.00

£16.00

£18.00

£20.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share

Danske

AIB

Bank of Ireland

Ulster (RBS)

Barclays

HSBCG

Halifax (LBG)

Santander

Nationwide

£0.00

£10.00

£20.00

£30.00

£40.00

£50.00

£60.00

0%-4.99% 5%-9.99% 10%-19.99% 20%-29.99%

Monthly price

Market share